On the backdrop of a sound and resilient financial system despite challenges, Zenith Bank Plc, Guaranty Trust Holding Plc (GTCO), and 10 other banks in Nigeria maintained stronger Liquidity and Capital Adequacy Ratios (CAR) in 2021.

Liquidity ratio is used to measure a company’s capacity to pay off its short-term financial obligations with its current assets, while CAR is a measure of how much capital a bank has available, which is reported as a percentage of a bank’s risk-weighted credit exposures.

The Central Bank of Nigeria (CBN) in 2021 required all banks to maintained liquidity ratio of 30 per, while other banking groups with international authorization and those that have been categorize as being Domestic Systemically Important Banks (D-SIBs) to maintain a minimum CAR of 15 per cent, while a minimum CAR of 10 per cent will be applicable to all other banks.

The apex bank in November 2021 set a deadline for banks to begin implementing Basel III criteria.

The Basel III standard is a voluntary global regulatory framework that addresses bank capital adequacy, stress testing, and market liquidity risk.

According to the CBN, the goal of the guidelines was to specify the minimum Liquidity Coverage Ratio (LCR) standards for reporting companies in the banking system.

The bank with stronger liquidity ratio and CAR comprises of; Zenith Bank Plc, United Bank for Africa Plc (UBA), Access Bank Plc, FBN Holdings Plc, Guaranty Trust Holding Plc, and Ecobank Transnational Incorporated (ETI).

Others are Stanbic IBTC Holdings Plc, Fidelity Bank Plc, Wema Bank Plc, Union Bank of Nigeria Plc, FCMB group Plc and Sterling bank Plc.

In the year under review, Zenith Bank leads other banks in liquidity ratio, while United Bank of Nigeria leads Tier-1 and Tier-2 banks in CAR.

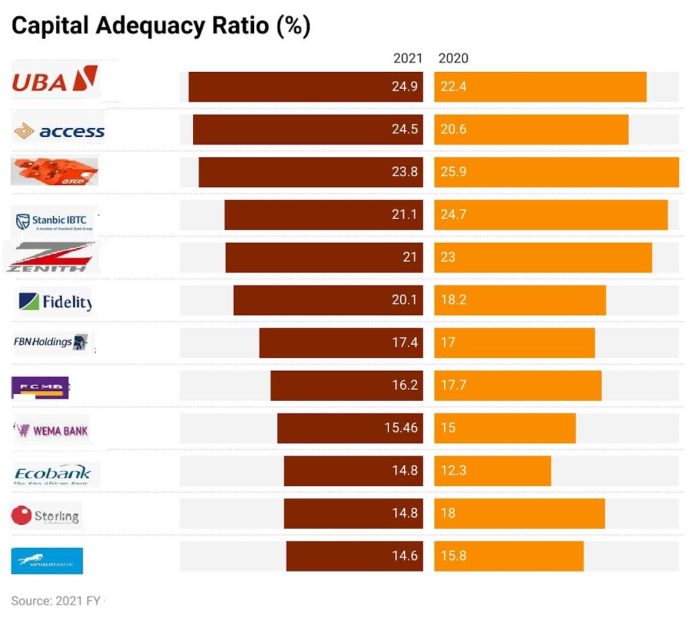

Findings by THISDAY revealed that Zenith Bank closed 2021 with a liquidity ratio of 71.6 per cent from 66.2 per cent reported in 2020. The group closed 2021 with CAR of 21 per cent, a decline of nine per cent from 23 per cent reported in 2020.

For UBA, it reported a liquidity ratio of 47.6 per cent in 2021 from 44.3 per cent in 2020, while CAR rose 24.9 per cent in 2021 from 22.4 per cent in 2020.

The members of the CBN Monetary Policy Committee (MPC) noted that the liquidity ratio remained well above its prudential limit at 41.3 per cent, though CAR declined marginally to 14.53 per cent in December 2021.

Speaking with THISDAY on Zenith Bank’s CAR as one of the highest in the banking sector, the vice president, Highcap Securities, Mr. David Adnori stressed that the statutory required liquidity ratio for banks is 30 per cent, maintaining that for Zenith Bank to have a liquidity ratio above 71.6 per cent is an interesting development in the banking sector.

He said, “If a bank has investment opportunities in the economy, a major portion of that fund that constitutes liquidity ratio is expected to be invested in such investments.

“That will yield income for the bank for increase shareholders’ returns on investment and expand the branch network.

“The bank can invest in government bonds, treasury and extend credit to customers. There are other areas of investment. However, if a bank has not done all these, it means Zenith Bank is holding a lot of liquid assets in its coffer.”

Meanwhile, Access Bank reported a 51 per cent liquidity ratio in 2021 from 46 per cent in 2020, while its CAR gained 3.9 per cent to close 2021 at 24.5 per cent from 20.6 per cent in 2020.

Access Bank was ahead of other banks in the implementation of Basel III with a successful issuance of $1 billion Eurobond in 2021.

Access Bank’s group managing director/CEO, Herbert Wigwe had maintained that the success of the transaction, which he said was the first in the Nigerian banking industry and the first of its kind in Africa outside of South Africa, would significantly enhance the bank’s tier-1 and total capital ratios in Nigeria.

While interacting with analysts on the bank’s 2021 financial year, the Group Chief Financial Officer, Access Bank, Mr. Seyi Kumapayi in a statement said, “On the liquidity side we’ve seen a liquidity ratio north of 50per cent. Foreign exchange liquidity is actually a lot more robust.

“We have a liquidity crisis in USD, which is not our functional currency. So it’s north of 50per cent at any point. Our loan to deposit ratio on our Dollar book is a maximum of 50per cent and we have always operated well below that.”

In addition to the Tier-1 banks ratio, GTCO reported a liquidity ratio closed H1 2021 at 44.71 per cent from 38.9 per cent, while FBN Holdings closed 2021 with a liquidity ratio of 17.4 per cent from 17 per cent reported in 2020.

GTCO in a presentation to investors/analysts said, “The Group continued to maintain strong capital positions with Full and Transitional IFRS 9 impact CAR of 23 8 per cent and 25 4 per cent respectively, 883 basis points above the regulatory minimum of 15per cent.

“Tier 1 capital remained a very significant component of the Group’s CAR standing at 23per cent representing 97per cent of the Group’s Full IFRS 9 impact CAR of 23 8per cent.

“The robust Capital position provides headroom for the Group to meet future expansion and capacity for additional risk taking. The Group’s Capital has been sensitized for Basel III compliance and found robust enough to meet the requirements for additional capital for conservation and Counter cyclical buffers.”

A group of analysts at GTCO in a report titled, “Nigeria macro-economy outlook for 2022”, said, “In view of the introduction of Basel III which provides for a more stringent capital regime where the strength and sufficiency of a bank’s Tier 1 capital will determine how much risk it can take, most banks will look to shore up their Tier 1 capital position. For context, the new framework allows for banks to raise Tier 1 capital through the issuance of Perpetual Bonds.

“We expect to see more banks tap into this mode of capital raising just like some Tier 1 banks did in 2021.

“Of concern, however, is the view of some analysts that the new capital guideline could knock off as much as 200 basis points from the full impact CAR of some banks.

“This could erase the capital buffers of these banks. We expect the apex bank to encourage banks with capital shortfalls to retain a sizeable position of their earnings. The apex bank could work out transitional arrangements that will assist banks whose capital position is below the regulatory minimum to gradually build capital over a 3 – 5-year period.”

In its 2021 banking sector, Afrinvest West Africa said CAR of selected Sub-Saharan Africa (SSA) (19.2per cent) and Brazil, Russia, India, China, and South Africa (BRICS) (17.2per cent) banks, recorded was above the eight per cent global regulatory minimum under the BASEL III, reflecting effective risk management during the pandemic.

However, African peers such as Egypt (21.7 per cent), Ghana (20.2 per cent) and South Africa (19.8 per cent) were better capitalised than the Nigerian banks (19.7per cent). In the BRICS region, the Nigerian banks fared better than their peers aside South Africa.